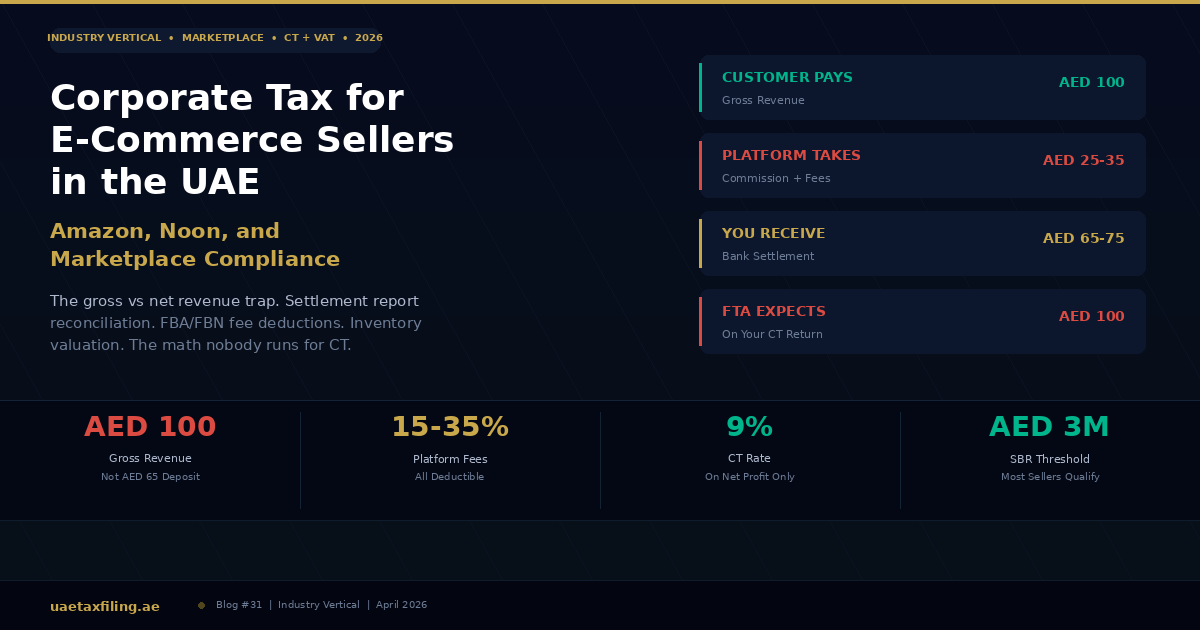

A customer pays AED 100 for a product on Amazon.ae. Amazon takes a 15% referral fee (AED 15), an FBA fulfillment fee (AED 9.50), storage fees (AED 1.20), and the closing fee (AED 1.30). The seller receives AED 73 in their bank account. When it comes time to file the corporate tax return, the seller records AED 73 as revenue. The FTA's automated systems compare that AED 73 against the AED 100 reported on the quarterly VAT return (because VAT is charged on the full AED 100 selling price). The numbers do not match. The mismatch triggers an audit flag.

This is the most common CT mistake among UAE marketplace sellers, and it happens because nobody explained the difference between gross revenue (what the customer paid), net settlement (what arrived in the bank), and the correct CT treatment (gross revenue minus separately disclosed marketplace fees). The taxable income is the same either way. The FTA's cross-referencing systems do not care about taxable income. They care about consistency between the revenue reported on the CT return and the revenue reported on the VAT return. If those numbers do not reconcile, your file gets flagged before a human reviewer ever sees it.

Our VAT for e-commerce guide covers the VAT side of marketplace selling in the UAE. This article covers the CT side: how to record marketplace revenue correctly for corporate tax, which platform fees are deductible and how to categorize them, how to value your inventory under IFRS, how to reconcile Amazon and Noon settlement reports against your CT return, and how the SBR election applies to marketplace sellers. If you sell on Amazon.ae, Noon, or any UAE marketplace and have never filed a CT return, this is the article that tells you what the FTA expects.

"Every marketplace seller we onboard has the same problem: their bank deposits do not match their revenue. That is not a bug. That is how marketplaces work. Amazon does not deposit AED 100 when a customer pays AED 100. They deposit AED 65 to AED 75 after deducting their fees. The seller treats the deposit as revenue and files it on the CT return. The FTA compares it to the VAT return and sees a 25-35% gap. That gap is the audit trigger."

Jazim, CEO, UAE Tax Filing LLC

The Gross vs Net Revenue Trap: The Most Common CT Mistake for Marketplace Sellers

When a customer buys a product on Amazon.ae for AED 100, the customer pays AED 105 (AED 100 product price + AED 5 VAT). Amazon collects the full AED 105. Amazon then deducts its fees (referral commission, FBA fees, storage, closing fees) and deposits the net amount in the seller's bank account. The seller sees AED 73 arrive. The natural instinct is to record AED 73 as revenue.

This is wrong for CT purposes. The correct treatment is to record the full AED 100 as gross revenue (excluding VAT, which is a pass-through and never appears on the CT return). The marketplace fees (AED 27 in this example) are recorded as separate, fully deductible business expenses. The taxable profit is identical either way: AED 100 minus AED 27 minus cost of goods sold minus other expenses equals the same net profit whether you record gross or net. The difference is how the FTA's automated systems see it.

As our 9 mistakes article documented, the number one automated audit trigger in UAE corporate tax is the mismatch between VAT return revenue and CT return revenue. For marketplace sellers, this mismatch is built into the business model. Your VAT return reports AED 100 in taxable supplies (the full selling price on which VAT is charged). If your CT return reports AED 73 (the bank deposit), the FTA sees a 27% revenue discrepancy. That triggers a review, even though the underlying profit is correct.

The fix is simple but specific: Record gross revenue (AED 100) on your CT return. Record each marketplace fee category as a separately disclosed deductible expense on the expenses schedule. The revenue on your CT return now matches the revenue on your VAT return. The marketplace fees are properly deducted. The taxable income is correct. The FTA's systems see consistency. No flag, no audit, no problem.

Which Marketplace Fees Are Deductible for CT (and Which Are Not)

Amazon.ae and Noon both deduct multiple fee categories from seller settlements. As Consultycs' marketplace guide documented, all fees are deducted before settlement, including referral commissions, fulfillment fees, return handling charges, and penalties. Every one of these carries 5% UAE VAT on top. Understanding which fees are deductible for CT and how to categorize them on the CT return is essential for accurate filing.

Fully deductible marketplace fees

Referral fees (commission). Amazon.ae charges 5% to 45% referral commission depending on product category, with most categories falling between 10% and 15%. Noon charges 5% to 30%. These are standard cost-of-sales expenses, fully deductible against CT revenue. Record them as 'marketplace commissions' or 'platform referral fees' in your expense schedule.

FBA and FBN fulfillment fees. Fulfillment by Amazon (FBA) and Fulfilled by Noon (FBN) charge per-unit fees based on product weight and dimensions. These cover picking, packing, and shipping. They are fully deductible as fulfillment expenses. Record them separately from referral fees so your P&L shows the true margin structure.

Monthly storage fees. Both platforms charge per-cubic-meter monthly storage fees for inventory held in their warehouses. These are fully deductible warehouse and storage costs. During Q4 peak season, Amazon applies higher storage rates, and long-term storage fees (LTSF) apply to inventory stored beyond 365 days. All deductible.

Advertising and sponsored product spend. Amazon PPC (pay-per-click) advertising, Noon Ads, and promoted listings are fully deductible marketing expenses. These should be recorded as advertising costs, not as marketplace fees, because they are discretionary spend rather than mandatory platform charges. The distinction matters for P&L analysis but not for CT deductibility. Our deductions guide covers the full rules on advertising expense deductibility.

Shipping and inbound freight. Costs to ship inventory to Amazon or Noon fulfillment centers, including customs duties paid on imported goods, are deductible as cost of goods sold (COGS) or separately as logistics costs. Import duties paid at customs become part of the landed cost of inventory and flow through COGS when the product is sold.

Fees that require careful treatment

Return handling fees. When a customer returns a product, the marketplace charges a return processing fee. This is deductible. However, the corresponding revenue reversal (the refund to the customer) must also be reflected in your books. A returned product reduces your gross revenue by the selling price and reduces your expenses by the return handling fee. Many sellers fail to record the revenue reversal, which overstates gross revenue and creates a VAT reconciliation issue.

Platform penalties and policy violations. Fines charged by Amazon or Noon for late shipments, policy violations, or customer complaint thresholds are categorized as fines and penalties. Under the UAE CT law, fines and penalties are non-deductible. As our deductions guide explained, this includes any fine regardless of who imposed it. A seller fined AED 500 by Amazon for late shipment cannot deduct that AED 500 on the CT return.

Seller subscription fees. Amazon's Professional selling plan (approximately AED 180/month) is a fully deductible business subscription expense. Record it as a software or platform subscription.

Recording marketplace fees correctly across 15-20 different fee categories is where most seller accountants make errors. Our accounting team categorizes every Amazon and Noon fee line by CT treatment (deductible, non-deductible, COGS, or operating expense) and reconciles your settlement reports against your CT return quarterly. Message us on WhatsApp.

Inventory Valuation: The CT Question Most Sellers Ignore

For a service business, revenue minus expenses equals profit. For a product business, the calculation has a third variable: inventory. The cost of goods sold on your CT return is not the total amount you spent on inventory during the year. It is the cost of the inventory you actually sold during the year. Unsold inventory sitting in an Amazon FBA warehouse or a Noon fulfillment center at the end of your financial year is an asset on your balance sheet, not an expense on your income statement.

Under IFRS (which is the mandatory accounting standard for UAE corporate tax), inventory must be valued at the lower of cost or net realizable value. Cost includes the purchase price, import duties, freight charges to bring the inventory to its present location, and any other costs directly attributable to acquisition. It does not include storage fees after the inventory arrives at the fulfillment center (those are period expenses, deductible in the quarter incurred) or advertising costs (also period expenses).

Why this matters for CT: A seller who purchased AED 500,000 in inventory during the year, sold AED 400,000 worth of it (at cost), and has AED 100,000 still in the FBA warehouse at year-end, has a COGS of AED 400,000, not AED 500,000. The AED 100,000 of unsold inventory is a current asset. If the seller deducts the full AED 500,000 as an expense, taxable income is understated by AED 100,000, which means CT is underpaid by AED 9,000 (AED 100K x 9%). This is not a rounding error. It is a common, material mistake that the FTA's audit systems can catch by comparing year-end inventory values against COGS patterns.

The inventory write-down question. If inventory becomes damaged, obsolete, or its market value drops below cost, IFRS requires a write-down to net realizable value. The write-down creates an expense that reduces taxable income. However, the write-down must be documented: the reason for the impairment, the evidence of reduced market value, and the calculation of the write-down amount. Amazon sellers with long-term storage inventory (365+ days) often face this issue when Amazon charges LTSF penalties and the inventory is effectively unsellable at the original cost.

The practical approach for small sellers: If you purchase and sell inventory in relatively consistent volumes and your year-end stock is small relative to annual sales, the inventory valuation adjustment may be minor. But if you import large batches seasonally (buying AED 300,000 in Q3 for Q4 holiday sales, for example), the year-end inventory value can significantly affect your CT calculation. Our year-end planning guide covers the August financial statement preparation step, which is where inventory valuation should be finalized before the September 30 CT filing deadline.

The Complete Marketplace Seller CT Calculation: AED 2 Million in Customer Orders

Here is the full walkthrough for a mid-sized Amazon.ae seller with AED 2 million in gross customer orders over a calendar-year financial period.

Revenue

Gross customer orders (excl. VAT): AED 2,000,000. This is the correct revenue figure for the CT return. Not the AED 1,400,000 bank deposit. Not the AED 2,100,000 including VAT. The VAT-exclusive customer order total as shown on the Amazon settlement summary report.

Cost of goods sold

Inventory purchased during the year: AED 900,000 (product cost + import duties + freight). Opening inventory: AED 80,000. Closing inventory: AED 120,000. COGS: AED 860,000 (AED 80K + AED 900K - AED 120K). Note: closing inventory is higher than opening, meaning some of this year's purchases are unsold and carried forward as an asset.

Marketplace fees (all fully deductible)

Referral commissions: AED 260,000 (13% average across categories). FBA fulfillment fees: AED 120,000. Monthly storage: AED 18,000. Closing fees: AED 8,000. Total marketplace fees: AED 406,000.

Other operating expenses (all fully deductible)

Amazon PPC advertising: AED 80,000. Product photography and listing optimization: AED 15,000. Office rent (or home office allocation): AED 36,000. Accounting and bookkeeping fees: AED 12,000. Shipping supplies and packaging: AED 8,000. Software subscriptions (inventory management, repricing): AED 6,000. Professional seller plan: AED 2,160. Total other operating expenses: AED 159,160.

CT calculation

Gross revenue: AED 2,000,000. Less COGS: AED 860,000. Gross profit: AED 1,140,000. Less marketplace fees: AED 406,000. Less operating expenses: AED 159,160. Net profit (accounting): AED 574,840. Less AED 375,000 zero-rate band: AED 199,840 taxable at 9%. Corporate tax payable: AED 17,986. Effective rate on gross revenue: 0.9%. Effective rate on net profit: 3.1%. Filing deadline: September 30, 2026 for calendar-year entities.

AED 17,986 in corporate tax on AED 2 million in customer orders. That is the real CT cost of running a UAE marketplace business. As ClearTax's UAE CT overview confirms, the standard rate of 9% applies only to taxable income above AED 375,000, and as PwC's tax summary documents, losses can be carried forward indefinitely to offset up to 75% of future taxable income. Sellers who hear '9% tax' and panic are overstating their liability by a factor of ten. Sellers who hear 'no tax in the UAE' and ignore CT entirely are underestating it by AED 17,986 plus the AED 10,000 late registration penalty plus 14% annual interest on the underpaid amount.

Small Business Relief: Most Marketplace Sellers Qualify

If your gross revenue (customer orders, not bank deposits) was under AED 3 million for the tax period, you are eligible for Small Business Relief. Electing SBR treats your taxable income as zero. No CT payable. For the seller in our worked example (AED 2M revenue), SBR would reduce the CT from AED 17,986 to AED 0.

SBR is available until tax periods ending December 31, 2026. For most marketplace sellers, this means the 2025 return (filed September 30, 2026) and the 2026 return (filed September 30, 2027) are both eligible. From 2027, SBR is no longer available and CT applies at the standard rate.

The trade-off, as our SBR analysis explained: electing SBR means no losses are recognized. If your business had a loss (expenses exceeded revenue), that loss cannot be carried forward to offset future profits. For a seller who invested heavily in inventory or advertising in 2025 and made a loss, SBR destroys the future value of that loss. For a profitable seller under AED 3M revenue, SBR is almost always the right choice because it eliminates the CT entirely at no real cost.

Revenue measurement for SBR: The AED 3M threshold is measured on gross revenue, not net settlement. A seller receiving AED 2.1M in bank deposits might think they are well under AED 3M. But if their gross customer orders (before marketplace fee deductions) were AED 3.1M, they are above the SBR threshold and owe CT at the standard rate. Always use the Amazon or Noon gross orders total, not the deposit total, to determine SBR eligibility.

How to Reconcile Your Settlement Reports Against the CT Return

Amazon.ae and Noon both provide detailed settlement reports that break down every transaction: gross sales, fees by category, refunds, adjustments, and net deposits. These reports are the bridge between what your marketplace dashboard shows and what your CT return should contain. The reconciliation process runs in three steps.

Step 1: Download the annual settlement summary. Amazon provides settlement reports per settlement period (typically biweekly). Download all settlement periods for your financial year and consolidate them into a single annual summary. The key line items are total product sales (gross), total fees by category, total refunds, total adjustments, and total deposits. For Noon, the seller portal provides a transaction report that can be exported and filtered by date range.

Step 2: Cross-check gross sales against VAT returns. Add up the gross product sales from the settlement summary. This should approximately equal the total taxable supplies you reported across your four quarterly VAT returns. If the numbers differ significantly (more than 5%), investigate: the most common cause is timing differences (a December sale settled in January, or a refund processed across quarters). Document every variance in a reconciliation memo. This is the same reconciliation process our year-end planning guide covers for May of the countdown timeline.

Step 3: Map settlement fee categories to CT expense categories. Amazon's settlement report lists fees generically (e.g., 'FBA fees,' 'referral fee,' 'storage fee'). Your CT return needs these categorized as COGS (import duties, freight, product cost), selling expenses (referral commissions, FBA fees, closing fees), storage costs (monthly and long-term storage), marketing expenses (PPC, sponsored products), and non-deductible items (penalties, policy violation fines). Create a mapping template that you reuse each quarter. Our accounting service maintains this mapping for every marketplace seller client as standard.

Settlement report reconciliation is the most time-consuming part of CT filing for marketplace sellers. We automate the process: downloading reports, consolidating across settlement periods, mapping fee categories, reconciling against VAT returns, and preparing the CT return schedules. Talk to us on WhatsApp.

Free Zone or Mainland for E-Commerce: The Decision That Determines Your Tax Structure

Our free zone vs mainland comparison covers this decision in depth. For marketplace sellers specifically, the answer depends on where your customers are located and how fulfillment works.

If you sell exclusively to international customers (cross-border e-commerce): A free zone structure with QFZP status can deliver 0% CT on qualifying income. Revenue from customers outside the UAE is qualifying income for QFZP purposes. However, if Amazon FBA fulfills orders from a UAE warehouse to UAE customers (which it does for most Amazon.ae orders), that revenue is UAE-source and likely non-qualifying. The QFZP benefit works primarily for sellers who export directly from their own warehouse to international buyers, not for sellers using FBA for domestic delivery.

If you sell to UAE customers through Amazon.ae or Noon: Your revenue is UAE-source. This is non-qualifying income for QFZP purposes. A free zone entity earning primarily non-qualifying income pays 9% CT on that income (with no AED 375,000 band on the non-qualifying portion) plus the mandatory QFZP audit cost (AED 15,000 to AED 40,000). A mainland entity pays 9% on all income above AED 375,000 and skips the mandatory audit. For most sellers with primarily UAE customers, the mainland structure is cheaper. As our free zone vs mainland article showed, the AED 540,000 profit crossover point is where the free zone stops being the better deal.

If your revenue is under AED 3M (most small marketplace sellers): Mainland with SBR is the clear winner until December 2026. CT = AED 0, no audit required, no income classification complexity. Once SBR expires, evaluate your actual numbers and restructure only if the math justifies the compliance cost.

Multi-Channel Sellers: Amazon + Noon + Own Website

Many UAE e-commerce businesses sell across multiple platforms simultaneously: Amazon.ae, Noon, their own Shopify or WooCommerce store, Instagram direct sales, and sometimes physical retail. Each channel has different fee structures, different settlement timing, and different VAT treatment. For CT purposes, all revenue from all channels is consolidated into a single return.

The challenge is reconciliation. Each platform reports revenue differently. Amazon provides settlement reports with fees netted. Noon provides transaction reports. Your own website processes payments through Telr, Stripe, or Network International with separate transaction fees. Direct sales may be invoiced manually. As BookkeepingExpert's compliance guide observed, poor preparation across multiple revenue channels can lead to penalties, incorrect tax liability, and cash-flow pressure. The CT return needs a single consolidated revenue figure that matches the sum of all VAT return figures across all channels.

For sellers managing multiple channels, a cloud accounting platform (Zoho Books, QuickBooks, Xero) with marketplace integrations is essential. The platform pulls settlement data from each channel, records gross revenue and fees separately, consolidates across all sources, and produces the unified P&L that forms the basis of the CT return. If you are managing this on spreadsheets, the risk of reconciliation errors compounds with every additional channel. Multi-channel sellers with more than AED 1M in combined revenue across platforms should seriously consider outsourced accounting to avoid the errors that trigger FTA audits.

The Related Party Trap for Marketplace Sellers

If you operate multiple companies that transact with each other in the e-commerce supply chain, transfer pricing rules apply. Common scenarios: a trading company imports goods and sells them to a separate company that lists and sells on Amazon, or the seller company pays a management fee to a company owned by the same person for warehousing, logistics, or administrative services.

These intercompany transactions must be at arm's length and disclosed on Schedule 5 of the CT return. If the trading company sells to the Amazon-listing company at an inflated price (to shift profits between entities), the FTA can adjust the transfer price. If the management fee between related entities is not at a rate that an independent party would charge, the FTA can reassess. For multi-entity e-commerce operations, TP documentation is not optional. It is a specific requirement that our transfer pricing guide covers in detail.

Five CT Mistakes Marketplace Sellers Make That the FTA Will Catch

1. Recording net bank deposits as revenue instead of gross customer orders. The most common and most consequential error. Creates a 25-35% gap between CT revenue and VAT revenue that triggers the automated audit flag.

2. Deducting the full inventory purchase as an expense instead of calculating COGS. Unsold inventory at year-end is an asset, not an expense. Deducting the full purchase cost understates taxable income and underpays CT.

3. Not registering for CT because the bank deposits are below AED 375,000. The registration threshold for juridical persons is AED 0 (all entities must register regardless of revenue). As Chambers & Partners' UAE corporate tax guide noted, no specific rules prevent individuals from incorporating to benefit from potential tax efficiencies. The AED 375,000 is the zero-rate band, not the registration threshold. The AED 10,000 late registration penalty applies per entity.

4. Using SBR eligibility based on net deposits instead of gross revenue. The AED 3M SBR threshold is measured on gross revenue (total customer orders), not the net amount deposited by the marketplace. A seller with AED 2.1M in deposits may have AED 3.1M in gross revenue and be ineligible for SBR.

5. Ignoring platform penalties as non-deductible. Late shipment fines, policy violation charges, and similar platform penalties are fines under the CT law and are non-deductible. Recording them as deductible expenses creates an incorrect return that the FTA's systems will catch during audit.

We handle CT filing for marketplace sellers end-to-end: settlement report reconciliation, gross vs net revenue correction, inventory valuation, fee categorization, SBR election modeling, and EmaraTax filing. The September 30 deadline for 2025 returns is approaching. Start the conversation on WhatsApp.

Frequently Asked Questions

Do Amazon and Noon sellers need to register for corporate tax in the UAE?

Yes. All juridical persons (LLCs, free zone entities) must register regardless of revenue. Natural persons (sole proprietors) must register if business turnover exceeds AED 1 million. Our freelancer CT guide covers the natural person registration process in detail.

Should I record gross revenue or net bank deposits on my CT return?

Gross revenue (total customer orders excluding VAT). Net bank deposits are not revenue. The difference between gross and net is marketplace fees, which must be recorded as separate deductible expenses.

Are Amazon FBA fees deductible for corporate tax?

Yes. Referral fees, FBA fulfillment fees, storage fees, closing fees, and seller subscription fees are all fully deductible business expenses. Platform penalties and fines are non-deductible.

How do I value my inventory for CT purposes?

At the lower of cost (purchase price + import duties + freight) or net realizable value, per IFRS. Unsold inventory at year-end is an asset on the balance sheet, not an expense deducted from revenue.

Can I use Small Business Relief as a marketplace seller?

Yes, if your gross revenue (not net deposits) is under AED 3 million per tax period and you operate on the mainland. SBR is not available to QFZPs in free zones. Available until December 2026.

Is a free zone better for e-commerce sellers?

Only if 100% of your customers are outside the UAE and you fulfill orders directly (not through FBA to UAE addresses). For sellers with UAE customers, mainland is usually cheaper after QFZP compliance costs.

How do I reconcile Amazon settlement reports with my CT return?

Download all settlement periods for the financial year, consolidate into an annual summary, cross-check gross sales against VAT returns, and map fee categories to CT expense categories.

What is the CT filing deadline for marketplace sellers?

September 30, 2026 for businesses with a calendar-year financial period ending December 31, 2025. Nine months after tax period end.

Do I owe CT if I sell on Amazon but make a loss?

No CT is payable on a loss. The loss can be carried forward to offset future profits (unless you elected SBR, which treats income as zero and does not recognize losses).

Can I deduct Amazon PPC advertising spend?

Yes. Advertising spend on Amazon PPC, Noon Ads, and any other platform advertising is fully deductible as a marketing expense.

Your Bank Deposit Is Not Your Revenue. Your Customer Order Is.

The entire CT compliance challenge for marketplace sellers comes down to one number: gross revenue. Record it correctly, and the rest of the CT return follows logically. Marketplace fees are deducted as expenses. Inventory is valued at cost or net realizable value. The AED 375,000 band reduces the taxable income. SBR may eliminate it entirely for sellers under AED 3M. The effective tax rate for a well-structured marketplace business is typically under 1% of gross revenue.

Record it incorrectly (using net deposits instead of gross orders), and you create the audit trigger that brings everything else into question. The FTA does not need to investigate your business model. It just needs to compare one number on your VAT return against one number on your CT return. If they do not match, your file gets flagged. For marketplace sellers, they will not match unless you understand the difference between what the customer paid and what the platform deposited.

Get the gross revenue right. Everything else follows.